Specializing in the research and production of high-end copper foil

5G copper foil

Category:

Keywords:

Product Description

- 产品描述

-

Electronic copper foil is one of the basic materials in the electronics industry. More than 90% is used in the production of copper-clad laminates. In recent years, new application areas have emerged, such as copper foil for the 5G industry, high-frequency high-speed PCB copper foil, and lithium-ion batteries.

5G Industry and Copper Foil Demand

It is estimated that the total 5G investment of China's three major operators is expected to exceed 1.3 trillion yuan, an increase of more than 60% compared to the 4G era. In the early stages of 5G commercial use, operators will carry out large-scale network construction, and the equipment manufacturing revenue brought about by 5G network equipment investment will become the main source of direct economic output of 5G. It is estimated that in 2020, the combined revenue of network equipment and terminal equipment will be approximately 450 billion yuan, accounting for 94% of the total direct economic output. In the mid-term of 5G commercial use, the expenditure on terminal equipment and telecommunication services from users and other industries will continue to grow. It is estimated that in 2025, the above two expenditures will be 1.4 trillion yuan and 0.7 trillion yuan respectively, accounting for 64% of the total direct economic output. In the later stages of 5G commercial use, the revenue from information services related to 5G from Internet companies will increase significantly, becoming the main source of direct output. It is estimated that in 2030, the revenue from Internet information services will reach 2.6 trillion yuan, accounting for 42% of the total direct economic output.

High-frequency PCB refers to signals in the millimeter-wave frequency band (0.3-3THz) of the "microwave" frequency band. Currently, 5G, automotive communication, and some consumer electronic products using PCBs are developing towards the millimeter-wave circuit field, and electronic copper foil will become one of the irreplaceable main raw materials.

Copper-clad laminate, also known as copper-clad laminate or copper-clad substrate (Copper Clad Laminate, abbreviated as CCL), is a key raw material for manufacturing printed circuit boards (PCBs), and is also a user and downstream product of electronic copper foil. FR-4 is the mainstream product of glass cloth-based copper-clad laminates, mainly used in high-end products such as computers, communications, and mobile phones. Although China has become the region with the largest output of copper-clad laminates in the world, the low-end boards mainly based on paper-based copper-clad laminates still account for a considerable proportion. The market prospects for mid-to-high-end copper-clad laminates such as FR-4 glass cloth-based laminates are broad, and the product added value is far higher than that of paper-based boards. Moreover, after years of development in China, production equipment and process technology have become more mature and stable.

As an emerging market for high-end copper foil, lithium battery copper foil has seen rapid growth in demand. According to national statistical data, it is predicted that by 2020, the domestic market share of electric vehicles will be no less than 5 million, and with an annual market input of 500,000 to 1 million vehicles, the amount of lithium battery copper foil used in electric buses and electric trucks is no less than 200 kg per vehicle, and the amount of lithium battery copper foil used in electric small passenger cars is no less than 30 kg per vehicle. The annual market demand for lithium battery copper foil for electric vehicles is approximately 90,000-150,000 tons, which is close to the amount used in the copper foil market for copper-clad laminates. Lithium batteries are not only widely used in mobile phones, laptops, electric vehicles, and electric bicycles, but also in aerospace, artificial satellites, and energy storage. Due to the advantages of small size, high capacity, and multiple charge and discharge cycles of lithium batteries, they have obvious advantages in the energy storage field of solving the imbalance of electricity consumption between peak and valley in the power grid. It is predicted that its market prospects can be comparable to the electric vehicle market. The broad development prospects of lithium batteries also bring huge development space to the lithium battery materials industry.

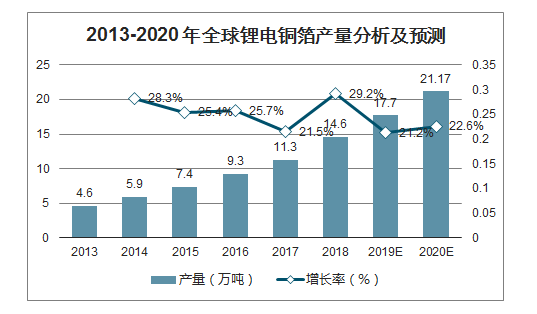

From a global perspective, in 2018, the global production of lithium battery copper foil increased by 29.20% year-on-year, reaching 146,000 tons. In the next few years, driven by the growth of the global lithium-ion battery market, especially the demand for lithium battery copper foil from power batteries, will maintain a high growth trend. The global lithium battery copper foil market will continue its high growth trend. It is estimated that the production will exceed 200,000 tons in the next four years, with a CAGR of 24%.

Analysis and Forecast of Global Lithium Battery Copper Foil Production from 2013 to 2020

Data Source: Compiled from Public Information

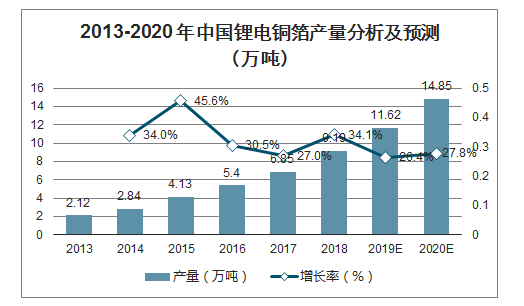

In 2019, China's lithium battery copper foil production was 116,200 tons. In the next few years, under the background of strong government support for the new energy vehicle industry, power batteries will drive the rapid growth of China's lithium battery copper foil market. It is estimated that by 2020, China's lithium battery copper foil production will reach 148,500 tons.

Analysis and Forecast of China's Lithium Battery Copper Foil Production from 2013 to 2020 (Ten Thousand Tons)

Data Source: Compiled from Public Information

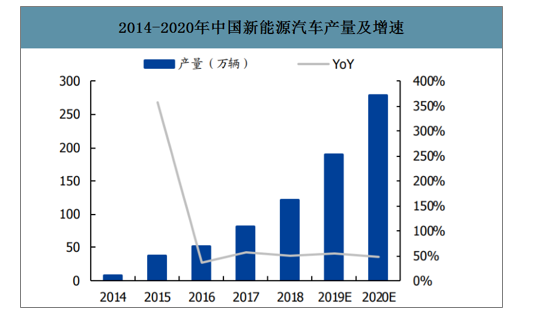

Production and Growth Rate of New Energy Vehicles in China from 2014 to 2020

Data Source: Compiled from Public Information

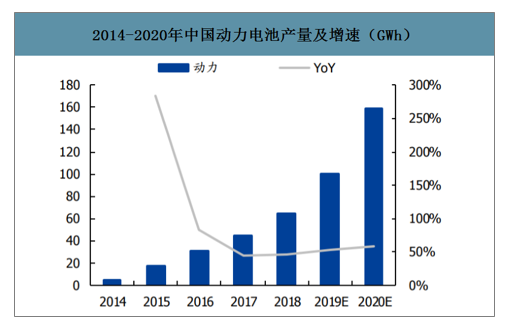

Production and Growth Rate of Power Batteries in China from 2014 to 2020 (GWh)

Data Source: Compiled from Public Information

Under the rapid development of the 5G industry, the production capacity of PCB copper foil has not yet seen rapid growth, but the PCB industry has been affected by the booming development of the 5G market. As an indispensable electronic component in the industry chain, the future demand for its raw materials CCL and PCB copper foil is very large, and the supply and demand situation of PCB copper foil will be marginally improved.

In the medium to long term, with the acceleration of the penetration rate of new energy vehicles and the higher demand for batteries in the 5G era, the demand for lithium battery copper foil will also increase significantly.

1.3 Copper-Clad Laminate Market Analysis

Copper-clad laminate, abbreviated as CCL, is the main upstream material for manufacturing printed circuit boards (PCBs). It is very important for the performance, quality, processability in manufacturing, and manufacturing cost of PCBs.

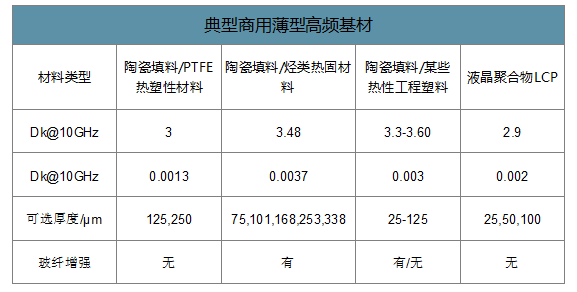

In order to meet the needs of high-frequency circuits, current copper-clad laminate manufacturers mainly improve the substrate materials from the following three aspects: Resin modification: using resin systems with lower polarity and smaller dielectric constant (Dk)/dissipation factor (Df); Glass fiber modification: Glass fiber reinforced materials are the main bearers of mechanical strength in composite materials. By reasonably mixing and matching different types of glass fibers, a balance between dielectric properties, processing properties, and cost can be achieved. Adjusting the PCB dielectric layer: In addition to modifying the substrate material itself, the dielectric properties of the substrate can also be improved by adjusting the distribution of multiple dielectric layers, that is, only low Dk/Df high-frequency materials are used in the dielectric layers that affect the transmission of high-frequency signals. Because the price of high-frequency substrates is much higher than that of conventional FR-4 substrates, the mixed-pressure laminated structure of high-frequency substrates and conventional substrates can effectively reduce costs. Currently commercialized high-frequency high-speed copper-clad laminate products include two major categories: thermoplastic and thermosetting, such as PTFE/ceramic filler substrates, hydrocarbon thermal/ceramic materials substrates, thermoplastic engineering plastics/ceramic filler substrates, LCP substrates, etc. (the possibility of new composite materials appearing in the future is not ruled out). When selecting specific types, processing manufacturers not only consider substrate loss but also the processability of the material itself. In the future, the diversification of PTFE fluoropolymers, hydrocarbon resins, and polyphenylene ether resins will become an evolutionary trend.

Typical Commercial Thin High-Frequency Substrates

Data Source: Compiled from Public Information

As the communications industry develops from low-frequency to high-frequency, the application market for high-frequency, high-speed copper-clad laminates is vast. In recent years, commercial applications have mainly focused on automotive electronic millimeter-wave radar. Driven by trends in automotive automation, electrification, entertainment, and networking, the penetration rate of driver-assistance systems is gradually increasing, leading to year-on-year growth in automotive radar shipments. This will continue to drive demand for ultra-high-frequency circuit substrates. This is a major "niche market" for suppliers with the capacity for mass production of related products before the arrival of the 5G large-scale investment period. The growth rate of this market is expected to increase significantly after the completion of 5G network construction. We estimate that the cumulative demand for high-frequency copper-clad laminate substrates from global automotive millimeter-wave radar will reach approximately 16.5 billion yuan from 2018 to 2025.

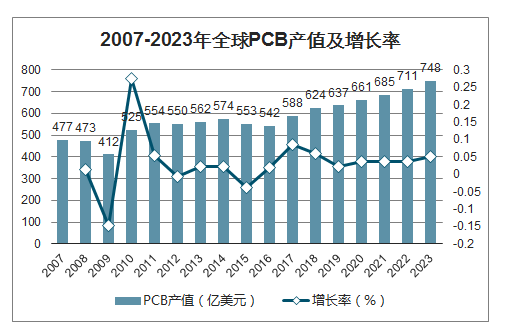

In 2018, the global PCB industry's total output value reached US\$62.396 billion, a year-on-year increase of 6.0%. It is predicted that the global PCB market will maintain moderate growth in the next five years, with the Internet of Things, automotive electronics, Industry 4.0, cloud servers, and storage devices becoming new drivers of PCB demand growth.

Global PCB Output Value and Growth Rate (2007-2023)

Data Source: Publicly Available Information

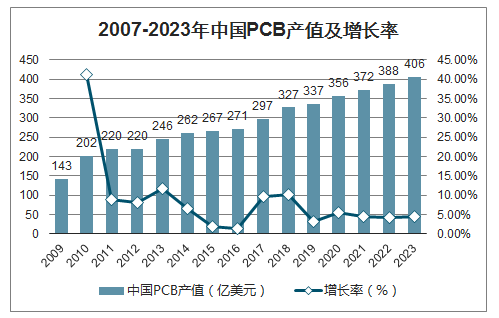

Benefiting from the global transfer of PCB production capacity to China and the booming manufacturing of downstream electronic terminal products, China's PCB industry has shown a rapid development trend. In 2006, China's PCB output value surpassed that of Japan, making China the world's largest PCB manufacturing base. Stimulated by strong demand growth in downstream sectors such as communication electronics, computers, consumer electronics, automotive electronics, industrial control, medical devices, and national defense and aerospace, China's PCB industry growth rate in recent years has been significantly higher than the global average. In 2018, China's PCB industry output value reached US\$32.702 billion, a year-on-year increase of 10.0%.

China's PCB Output Value and Growth Rate (2007-2023)

Data Source: Publicly Available Information

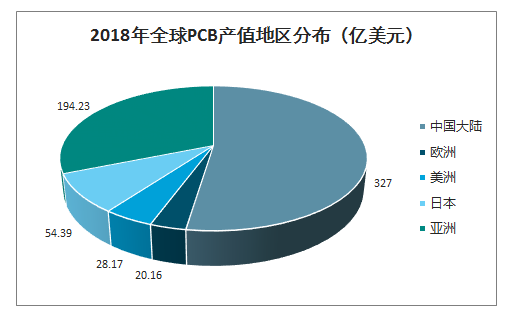

Global PCB Output Value Distribution by Region in 2018 (US$)

Data Source: Publicly Available Information

The PCB industry in mainland China has already accounted for half of the global market. In 2017, mainland China's PCB production accounted for more than 50% of the global total, making it a dominant force in the industry. Meanwhile, the scale of the PCB industry in the US, Japan, and Europe is shrinking. Mainland China, with its lower labor costs and government investment attraction policies, is expected to further increase its share in the future. The eastward shift of the PCB industry continues. As the technical capabilities of mainland China's PCB manufacturers improve, the gap with foreign companies will gradually narrow. Judging from the expansion pace of PCB manufacturers, most of the capacity increase in the next 1-3 years will come from domestic manufacturers. Taiwanese PCB companies have relatively less capacity expansion in this process, and leading domestic manufacturers may lead the growth of PCB output value in mainland China.

Leave a message

We attach great importance to your opinions and inquiries. If you have any questions about our products and services, please fill out the following form, and we will contact you as soon as possible.

The company has gathered a group of technical and management teams with 20-30 years of experience in electrolytic copper foil production.

Gan Public Security Network Security Permit No. 36080202000414

Quick Navigation

Products & Applications

Jiangxi Hongye Copper Foil Co., Ltd.

Tel:0796-8937778

Email:754678436@qq.com

Address: Jiyang Avenue, Industrial Park, Jizhou District, Ji'an City, Jiangxi Province